When FEMA announces a disaster declaration, most people think about emergency help and cleanup. However, for property owners, the effects often go much further. A recent FEMA disaster declaration has quietly changed how flood risk is reviewed across the area. Because of this, more homeowners, buyers, and lenders now ask for a FEMA Elevation Certificate, sometimes without much notice.

This change is not just about paperwork. Instead, it reflects how FEMA, insurance companies, and lenders respond after storms, flooding, and heavy runoff. Knowing what is happening now can help property owners avoid delays, higher insurance costs, and stalled projects later.

FEMA disaster declarations lead to long-term reviews

After a disaster declaration, FEMA does more than inspect damaged homes. It also studies how water moved, where it collected, and which areas came close to flooding. Even properties that stayed dry can face closer review.

In San Diego, this matters because the land changes quickly. Coastal areas, canyons, valleys, and hills all react differently to heavy rain. Once FEMA steps in, agencies and insurers often double-check whether current flood data still makes sense.

Because of this, elevation information becomes more important than before.

Flood risk looks different after a major storm

Before a disaster, flood zones can feel like lines on a map. After one, those lines feel real. FEMA uses data from the event to see how water flowed and which areas may face future risk.

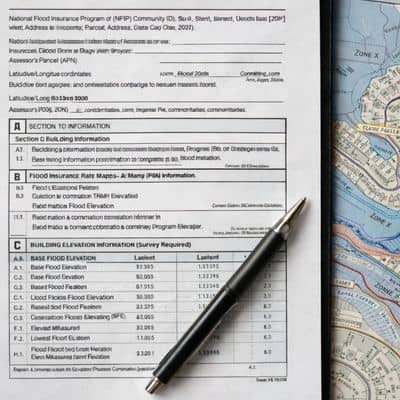

As a result, homes near flood zone edges often receive extra attention. Even a small difference in height can change how risk is labeled. That is where a FEMA Elevation Certificate helps. It gives clear proof of how high a building sits compared to flood levels.

Without this proof, reviewers often assume higher risk.

Why demand for FEMA Elevation Certificates is rising now

After a FEMA disaster declaration, several things happen at the same time.

First, insurance companies review policies more closely. They often ask for updated flood information before renewing coverage or changing rates. Next, lenders become more careful, especially during refinances. They want proof that a property meets flood rules.

At the same time, cities and counties tighten permit reviews. Repairs, additions, and rebuilds may now need stronger documents than before.

Because of all this, many property owners find themselves needing a FEMA Elevation Certificate.

San Diego property owners feel the impact right away

Many owners do not realize they need updated elevation data until something stops moving. For example, an insurance renewal may pause while the company asks for proof of elevation. In other cases, a refinance slows down because a lender wants flood details confirmed.

Home sales can also face delays. Buyers often hesitate when flood questions come up late in the process. Permits may also take longer if flood risk needs review.

These problems feel frustrating because the property itself may not have changed. Still, after a FEMA declaration, the review process often does.

Older elevation records may no longer be enough

Some property owners already have elevation documents from years ago. Sadly, those records do not always solve today’s issues.

FEMA disaster reviews can show gaps in older data. Flood maps change over time. Measurement standards also improve. In some cases, older certificates miss details now required by insurers or local agencies.

Because of this, reviewers may reject old documents or ask for updates. While this surprises many owners, it reflects FEMA’s push for better accuracy after a disaster.

Timing becomes a hidden problem

Another challenge appears when demand increases: timing. After a FEMA declaration, many people request elevation certificates at once. This rush can lead to longer wait times.

When deadlines get close, delays add stress. Insurance renewals, loan closings, and permits do not pause just because paperwork takes longer. Acting early helps avoid last-minute pressure.

On the other hand, waiting until someone demands a FEMA Elevation Certificate often limits choices and creates problems.

Proactive owners stay ahead

Some property owners take a different path. Instead of waiting, they check their flood documents early. By doing this, they handle questions before insurers, lenders, or buyers raise concerns.

An updated FEMA Elevation Certificate gives owners peace of mind. It shows exactly where a building stands and reduces confusion during reviews. In many cases, it also helps when discussing insurance costs or flood risk.

Rather than feeling forced, proactive owners stay in control.

FEMA’s recent action points to bigger changes ahead

Disaster declarations often lead to lasting updates. Over time, flood maps change, rules tighten, and paperwork becomes more detailed.

This trend means elevation data will matter more in the future. As San Diego continues to see heavy rain and runoff, clear elevation records help protect property value and project timelines.

A FEMA Elevation Certificate is becoming a common request after major weather events, not a rare one.

A new reality for property owners

FEMA’s recent disaster declaration did more than bring emergency support to San Diego. It also started a chain reaction that affects insurance, lending, and permits.

For many owners, the rising demand for a FEMA Elevation Certificate comes as a surprise. Still, understanding why it happens makes it easier to manage.

Today, this certificate is more than a form. It is a practical tool that helps property owners move forward with confidence after a disaster.